Precious Metals Pullback as Oil Dominates Headlines

12 March 2026

Precious metals markets remain volatile as investors navigate an increasingly complex geopolitical and macroeconomic landscape. Prices have eased this week, with gold at the time of writing trading just below USD $5,200 per troy ounce (oz) while silver has fallen below $86oz, driven by an almost 3% correction overnight.

Despite recent price movements, both metals have delivered strong performance in 2026 to date. Gold is up approximately 19%, while silver has advanced by closer to 20%.

The gold-to-silver ratio currently sits at 58:1, broadly unchanged from the start of the year and remains close to its long-term historical average.

Market volatility intensified following the escalation of conflict between Israel and Iran on February 28. Despite rising in the immediate aftermath of the conflict starting, gold is lower now than when it started, with prices off by close to 3%.

Rather than representing a failure by gold to act as a safe haven asset, the move we have seen this month has been driven by investors temporarily rotating into the US dollar, which in the short-term is also a traditional haven asset in times of crisis.

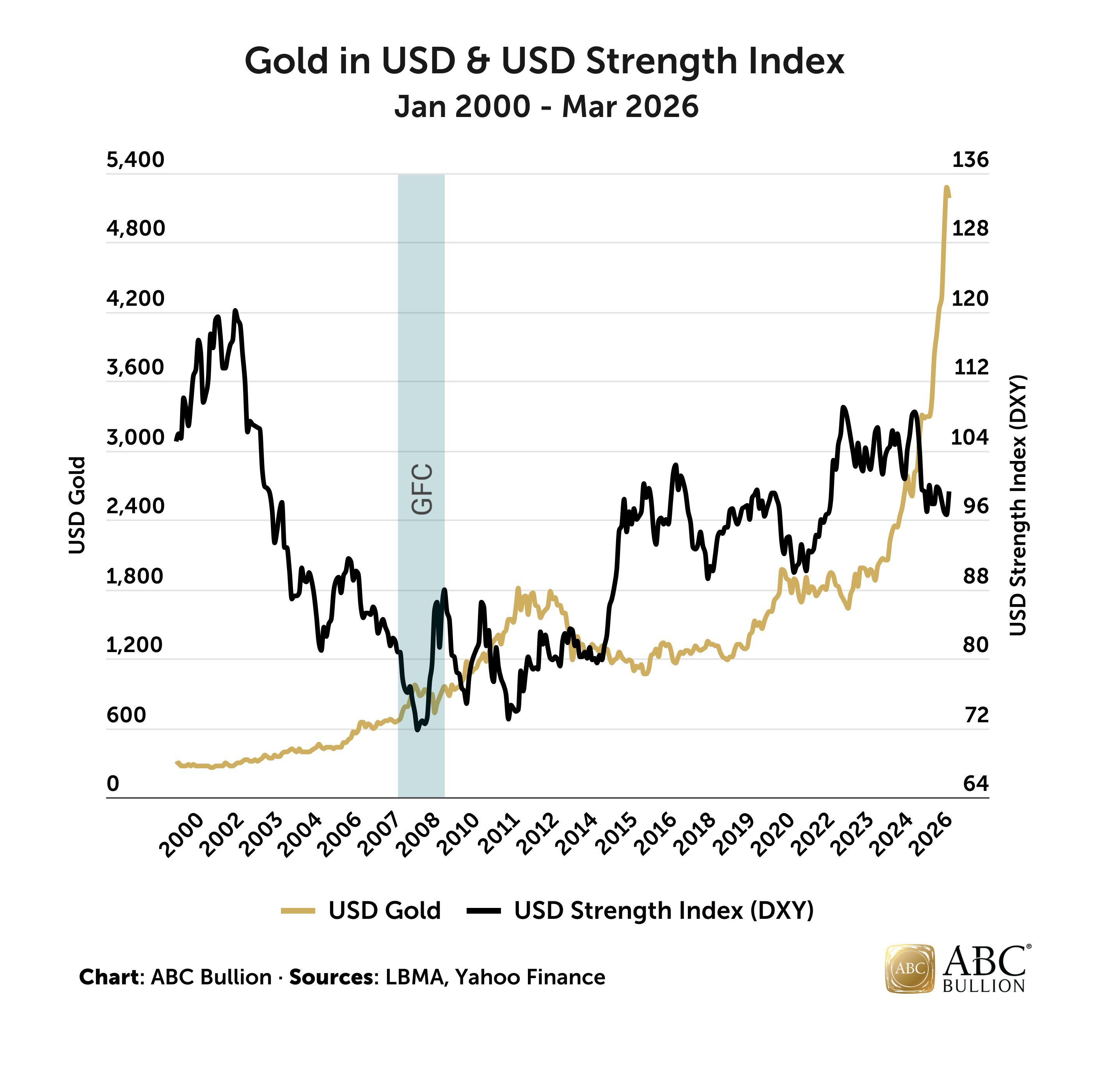

This shift is reflected in a notable rise of the US Dollar Index (DXY), which climbed from pre-conflict lows of 96.61 to recent highs of 99.32 (+2.8%). Historically, the two assets have exhibited an inverse relationship, thus, the recent strengthening in the dollar has been a key factor contributing to the short-term pullback in precious metal prices.

This has happened several times in the past 25 years, including when the Global Financial Crisis hit almost two decades ago. Gold originally sold off as investors scrambled for any liquidity they could get (there is a saying that in a crisis you sell what you can sell, not what you want to sell, with gold’s exceptional liquidity and total absence of credit risk making it one of the easiest assets to trade globally) before surging from 2009 to 2011 as policymakers flooded the markets with stimulus as depicted in the figure below.

Figure 1

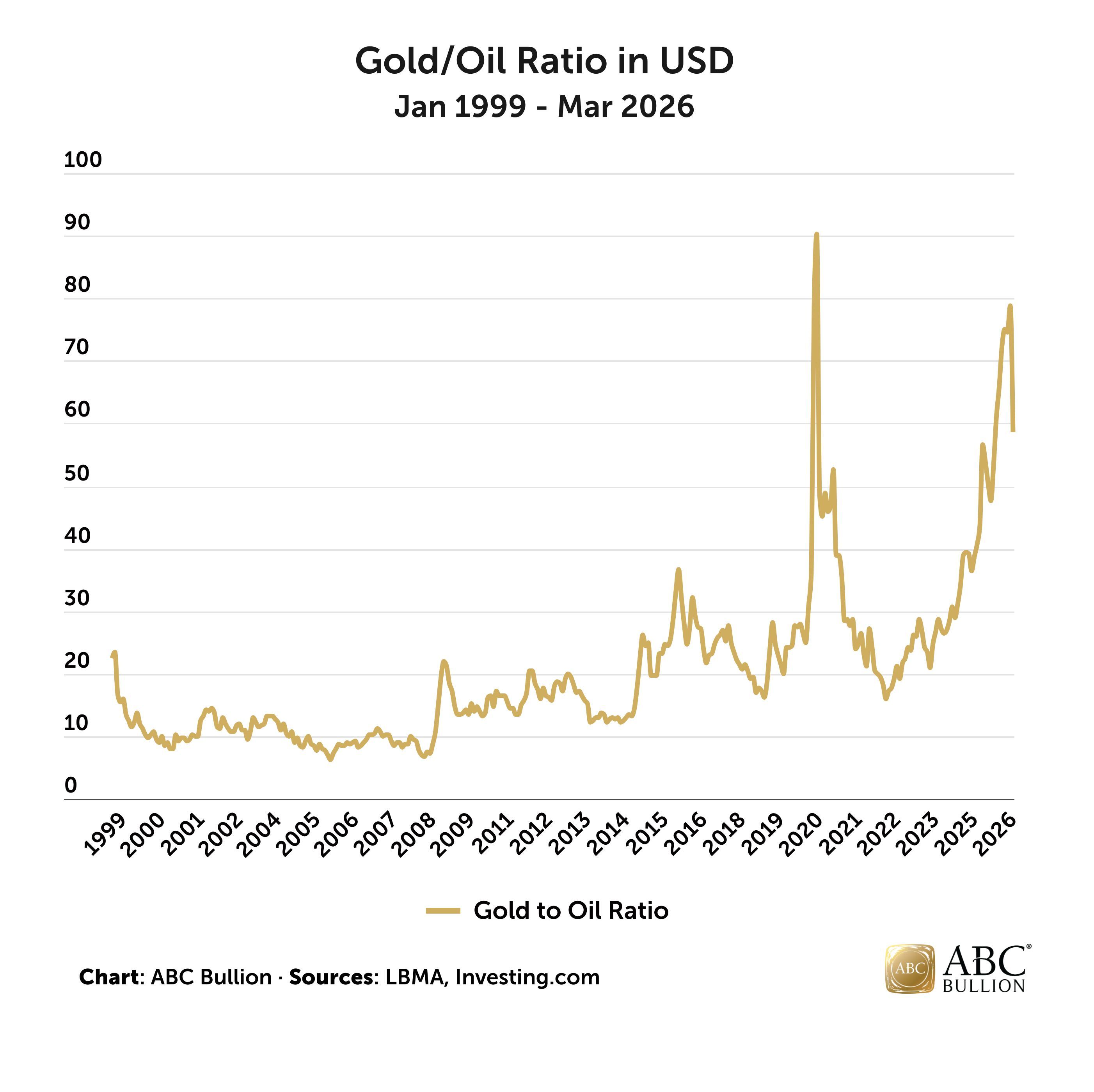

Energy markets have also experienced significant turbulence in recent days. Crude oil surged following reports that Iran had closed the Strait of Hormuz, one of the most critical energy transit corridors globally. The strait handles approximately 21% of global petroleum liquid consumption and around 20% of global LNG trade, making any disruption highly supply-side significant for global energy markets.

Oil prices briefly spiked to approximately USD $120 per barrel on March 9, representing a 91% increase from pre-conflict levels. This triggered renewed concerns over inflationary pressures and led markets to reassess larger expectations for interest rate cuts by the Federal Reserve mid year. This surge oil prices drove the gold-to-oil ratio significantly lower, falling from recent February highs of around 78 down to approximately 58 currently, as illustrated in Figure 2 below.

Figure 2

The prospect of falling rates in the US provides a highly supportive environment for precious metals, as investors shift away from lower yielding assets like cash and bonds toward assets with higher capital growth potential. However, the combination of a stronger US dollar and renewed uncertainty surrounding the interest rate outlook has weighed on prices in the near term.

Technically, gold continues to trade within a broad range, with key resistance emerging near the USD $5,200oz level for gold and around USD $90oz for silver. A sustained breakout above these levels would likely require a clearer macro picture, entailing either a renewed weakening in the US dollar or stronger signals that global monetary policy will shift toward easing.

In the short-term, there is also the potential for a further decline in prices, with both metals still trading well above their 200 day moving averages (200DMA). Should either gold or silver fall toward those averages, we would expect to see a surge in dip buying, as retreats to those price levels have proved excellent buying opportunities on several occasions in the past decade.

Looking ahead, event risk around Iran is likely to dominate global headlines, and price movements across risk assets, currencies and commodities. If oil stays bid—and decisively reclaims USD $100 a barrel or more—it will radically alter inflation expectations across the market.

It will also exacerbate the risk we enter a ‘stagflationary’ era not unlike that which we saw in the 1970s, with gold and other hard assets the standout performers throughout that period.

There is also a possibility the conflict ends sooner than expected, something US President Donald Trump has alluded to. That alone led oil prices to retreat toward USD $85 per barrel, easing immediate inflation concerns and potentially improving the outlook again for interest rate cuts later this year.

The uncertainty surrounding global trade and geopolitics is unlikely to end soon and should help keep precious metals supported.

With central bank purchasing robust, bar and coin demand strong, and ETF accumulation likely to persist, gold and silver continue to play a critical role as strategic portfolio holdings in an increasingly uncertain global environment.

Thank you for choosing ABC Bullion

Jordan Eliseo

General Manager, ABC Bullion

Luke Tyler

Market and Business Analyst, ABC Bullion

Disclaimer: This document has been prepared by Australian Bullion Company (NSW) Pty Limited (ABN 82 002 858 602) (ABC). The information contained in this document or internet related link (collectively, Document) is of a general nature and is provided for information purposes only. It is not intended to constitute advice, nor to influence any person in making a decision in relation to any precious metal or related product. To the extent that any advice is provided in this Document, it is general advice only and has been prepared without taking into account your objectives, financial situation or needs (your Personal Circumstances). Before acting on any such general advice, we recommend that you obtain professional advice and consider the appropriateness of the advice having regard to your Personal Circumstances. If the advice relates to the acquisition, or possible acquisition of any precious metal or related product, you should obtain independent professional advice before making any decision about whether to acquire it. Although the information and opinions contained in this document are based on sources, we believe to be reliable, to the extent permitted by law, ABC and its associated entities do not warrant, represent or guarantee, expressly or impliedly, that the information contained in this document is accurate, complete, reliable or current. The information is subject to change without notice, and we are under no obligation to update it. Past performance is not a reliable indicator of future performance. If you intend to rely on the information, you should independently verify and assess the accuracy and completeness and obtain professional advice regarding its suitability for your Personal Circumstances. To the extent possible, ABC, its associated entities, and any of its or their officers, employees and agents accepts no liability for any loss or damage relating to any use or reliance on the information in this document. It is intended for the use of ABC clients and may not be distributed or reproduced without consent. © Australian Bullion Company (NSW) Pty Limited 2020.